Our weekly roundup of tax-related investment strategies and news your clients may be thinking about.

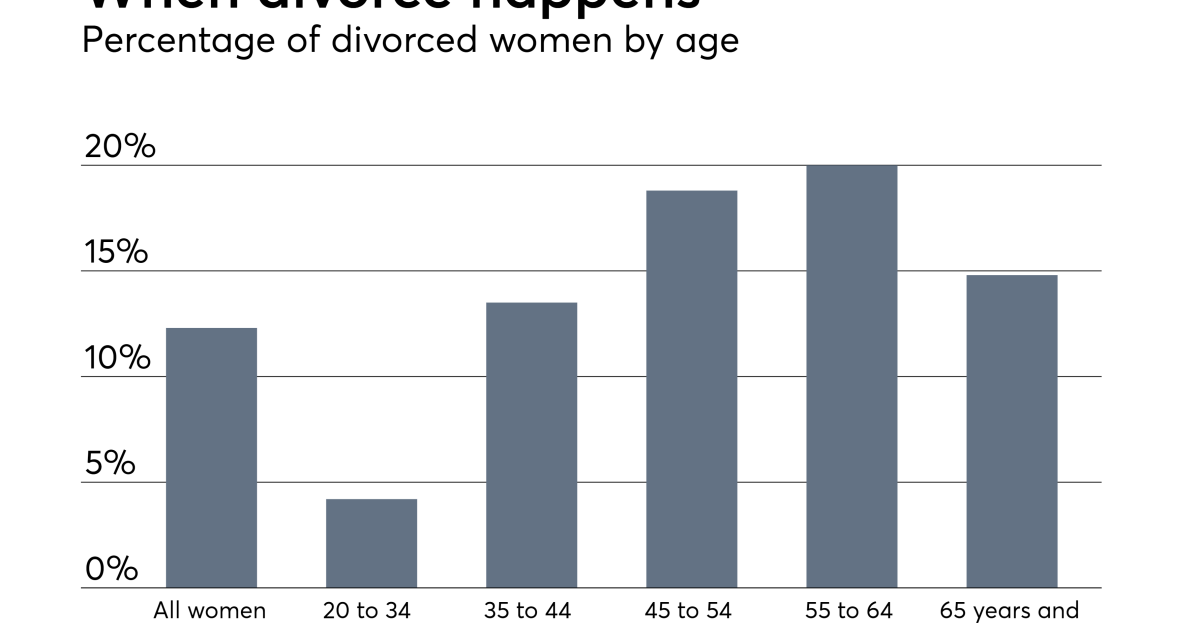

The new tax-deferred way of paying alimony

According to this CNBC article, alimony payments in divorce proceedings will no longer be deductible starting next year due to the new tax law. One way for the higher-earning spouse to save on taxes is to contribute to an IRA as support, suggests Ed Slott, a financial planning author and IRA distribution expert. “When the husband gives the IRA to his ex-wife, he is giving money that he would have paid taxes on,” Slott says. “He actually gets a deduction.”

How homeowners win and lose under the new tax law

Even though customers may be able to get tax breaks for buying a home, the savings will not be as great before the new tax law is passed, an expert writes on MarketWatch. While some of the tax breaks associated with homeownership remain, the new law has increased the standard deduction, making the itemizing through which clients can receive these tax breaks less valuable, the expert writes. However, home ownership can still be a good option as customers may receive a significant capital gains tax exclusion if they sell their home and meet all the requirements.

“Dying at your desk is not a retirement plan”

According to this Washington Post article, clients are advised to plan for their retirement because they risk not being able to retire at all. Older workers who have not yet built up a nest egg should start saving as soon as possible, reduce their spending and maximize contributions to their tax-advantaged retirement accounts. Creating a guaranteed source of income, such as a pension, is a good hedge against the risk of running out of savings in retirement. You should act now because “dying at your desk is not retirement planning,” says one advisor.

Investment tips for your Roth IRA

According to this article on Nasdaq, investors can maximize the benefit of an IRA's tax-deferred growth by parking investments that are subject to high tax rates in the account. For example, clients may place stocks in a Roth IRA for short-term investment because tax rates on short-term capital gains are higher than long-term rates. REITs are also good candidates for IRAs because REIT dividends are subject to ordinary income tax rates, which are higher than those on long-term capital gains.

401(k) Investors: Follow the 5% Rule to Protect Your Retirement

Clients investing in 401(k)s should avoid holding more than 5% of their total portfolio value in a single stock to ensure they remain on track to achieve their retirement goals regardless of market conditions, writes one USA Today expert. When selling a large position, “a gradual plan to sell may make sense” to minimize the tax burden, but one should first consider the impact of embedded capital gains, the expert explains. “If the stock falls before you sell, you may not have any profits to worry about later. I’ve seen a lot of losses caused by people trying to avoid taxes.”

Comments are closed.